InterviewSolution

Saved Bookmarks

InterviewSolution

This section includes InterviewSolutions, each offering curated multiple-choice questions to sharpen your knowledge and support exam preparation. Choose a topic below to get started.

| 2701. |

ajay , binayand chetanwerepartnerssharingprofirtsin theratio of3:3:2the partnershipDeedprovidedfor thethe following: (i) salary OfRs. 2,000 perwuaterto ajayand Binay . ( ii)chetanwasentitled to a commissionof Rs. 8,000 (iii)Binary was gurranteeda profitofRs. 50,000p.athe profitof thefirmforthe yearended31stMarch, 2015was Rs. 1,50,000whichwasdistributedamong ajayBinaryandchetanin theratioof 2:2:1 withouttakingintoconsiderationtheprovisionsof partnershipDeed ,passnecessaryrectifyingentry for theaboveadjustmentin thefirmshow yourworkingsclearly . |

|

Answer» |

|

| 2702. |

Akanksha Enterprises Ltd. Issued 12,000, 6% Debentures of Rs.100 each on September 1, 2009 redeemable at a premium of 7% as under : "On March 31, 20154,000 Debentures""On March 31, 20163,000 Debentures" "On March 31, 20175,000 Debentures" The Board of Directors has also decided to transfer the required amount to Debentures Redemption Reserve in four equal annual instalments starting with March 31, 2011. Record necessary journal entries. Ignore entries for interest. Investment as required by law was made in fixed deposite of the bank. |

Answer» SOLUTION :

|

|

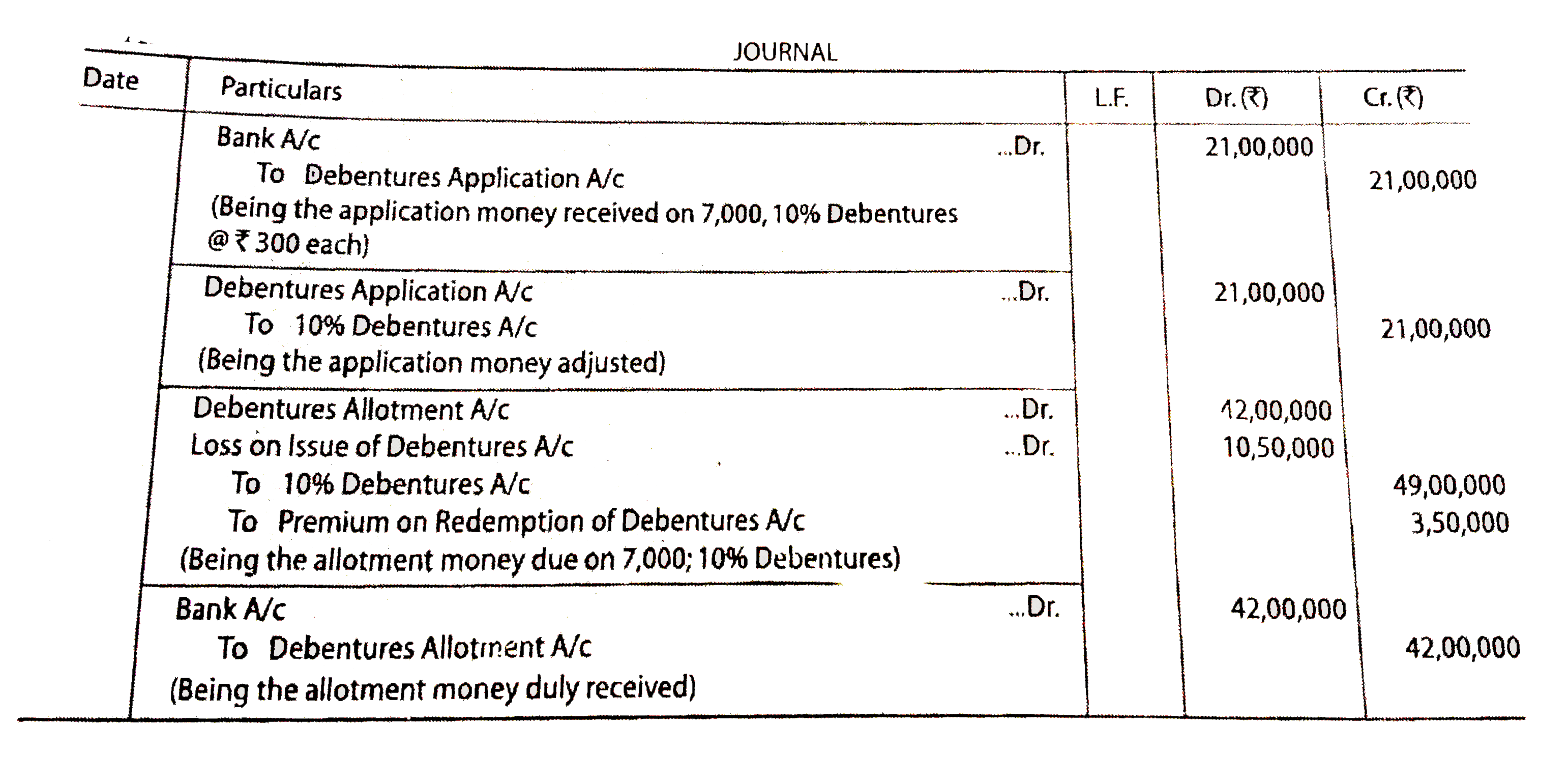

| 2703. |

Aishwarya Ltd. issued 7,000, 10% Debentures of Rs. 1,000 each at a discount of 10%, redeemable at a premium of 5% after 4 years. According to the terms of issue Rs. 300 was payable on a application and balance on allotment of debentures. Record necessary entries regarding issue of 10% Debentures. |

Answer» SOLUTION :

|

|

| 2704. |

Ajayandvijayare partners sharingprofitsin theratioin theof 3:2ajayis non- Workingpartner andcontributes Rs. 20.00.000as hiscapital Vijay is a working partner offirm, thepartnershipDeedprovidesfor interest on capital @ 8%and salarytoevery workingpartner@ 8.000permonths profit beforeprovidingforintereston capital andpartners 'ssalaryforthethey yearended31st March 2019 Was Rs. 80.000 showthedistribution of profit. |

Answer» Solution : intereston ajay's capital = RS. 20.00.000`xx`8/100=Rs,1.60.000, Salary toVijay = Rs. 8.000 `xx` 12 =Rs. 96.000, thusinterest n ajaycapitalot VIJAY`=Rs. 1.60.000 + Rs. 96.000=Rs. 2.56.000` sincebothintereston capitaland salarytopartnersareappropriationsand theprofitavailablefordistributionis Rs,80.000i.e.,lessthanamountof APPROPRIATIONSTO bemadetheavialableprofiitisdistributedin THERATIOOF approaritionsto beajayi.e.,1.60.000 (intereston capital ): 96.000 (salary )or5:3 |

|

| 2705. |

AFCONs India Ltd. (an infrastructure company) issued 5,00,000, 9% Debentures of Rs.20 each on April 1, 2005 redeemable on March 31, 2015. Investment as required by law was made in fixed deposit of the bank on 30th April. Record journal entries for issue and redemption of debentures. |

|

Answer» Solution :Debenture Redemption Reserve Created for Rs.25,00,000 on 31st March, 2014. Debenture Redemption Investment Rs.15,00,000 MADE on 30TH April, 2014. Note : As per new guidelines, INFRASTRUCTURE COMPANIES are also required to create DRR @25% of the nominal VALUE of debentures issued. |

|

| 2706. |

After transferring liabilities like creditors and bills payables in the Realisation Account, in the absence of any information regarding then payment, such liabilities are treated as: |

|

Answer» Never paid |

|

| 2707. |

Adjustment for Proposed Divident is |

|

Answer» Add previous years' PROPOSED dividend under net profit before tax and extra-ordinary ITEM and deduct it under FINANCING Activity |

|

| 2708. |

Adjustment for Proposed Dividend is : |

|

Answer» Add previous YEAR ' proposed dividend under net profit before TAX andextra - ordinary items and DEDUCT it under Financing Activity. |

|

| 2709. |

Accumulated profits on the retirement of a partner are |

|

Answer» Credited to all Partners' Capital Accounts in old PROFIT - SHARING ratio. |

|

| 2710. |

Accumulated losses are transferred to—— (Current/Capital Accounts) in —— (equal ratio/profit sharing ratio). |

|

Answer» |

|

| 2711. |

Accumulated Dividend Arrears' on preference shares is shown in the Company's Balance Sheet as : |

|

Answer» CURRENT Liability |

|

| 2712. |

Accounting ratios ignore qualitative factors and are also not compartable if different firms follow different policies comment. |

| Answer» | |

| 2713. |

Accountantof thefirmhasdebitedintereston partner'sloanto theprofitandLossappropriationAccountandcreditedtito thepartner's CapitalAccountActionof theAccountantis notcorrect,Why ? |

| Answer» Solution :Actionof theaccountantis notcorrectbecauseintereston loanis achargeaginst profit and not anappropriationof profitand alsoit ISA GAIN to a partnersas a lenderand not ASA partnersalsoat thetimeof dissoluionof THEFIRM, partners's loanis payablebeforecapitalis repaidHence, itshould have beendebited to profitand lossaccountandcreditiedtopartners 's Loanaccount . | |

| 2714. |

According to the guidelines issued by Securities and Exchange Board of India (SEBI) what percentage of the amount of debentures must be transferred to 'Debentures Redemption Reserve' before the commencement of redemption of debentures, in case of convertible debentures? |

|

Answer» 0.25 |

|

| 2715. |

According to the guideliness issued by Securities andExchange Board of India (SEBI) what percentage of the amount of debentures must be transferred to 'Debentures Redemption Reserve' before the commencement of redemption of debentures, in case of convertible debentures? |

|

Answer» A - 0.25 |

|

| 2716. |

According to prescribed order of assets in a Company's Balance Sheet ............. Assets should be shown first of all. |

|

Answer» Non-CURRENT ASSETS |

|

| 2717. |

Abhay and Beena are partners in a firm. They admit Chetan an a partner with 1/4th share in the profits of the firm. Chetan brings Rs 2,00,000 as his share of capital. The value of the total assets of the firm is Rs 5,40,000 and outside liabilities are valued Rs 1,00,000 on that date. Give necessary entry to record goodwill at the time of Chetan's admission. Also show your working notes. |

|

Answer» Solution :Value of CHETAN's SHARE in Firm's Goodwill: RS 40,000, Dr. Chetan's Capital A/c, Rs 40,00, CR. Abhay's Capital A/c, Rs 20,000 and Beena's Capital A/c: Rs 20,000. |

|

| 2718. |

Abha and Bimal are partners in a firm sharing profits and losses in the ratio of 3:2. On 31st March, 2015 they admitted Chintu into partnership for 1/5th share in the profits of the firm. On that date their Balance Sheet stood as under: Chintu was admitted on the following terms: (i) He will bring Rs 80,000 as capital and Rs 30,000 for his share of goodwill premium. (ii) Partners will share future profits in the ratio of 5:3:2. (iii) Profit on revaluation of assets and reassessement of liabilities was Rs 7,000. (iv) After making adjustments, the Capital Account of the partners will be in proportion to Chintu's capital. Balance to be paid off or brought in by the old partners by cheque as the case may be. Prepare the Capital Accounts of the partners and Bank Account. |

|

Answer» Solution :Sacrificing Ratio of Abha and Bimal `=1:1,` Amount of Goodwill BROUGHT by Chintu to be shared equally. Abha and Bimal will get Rs 15,000 each. PARTNERS' Capital Accounts: Abha- Rs 2,00,000, Bimal-Rs 1,20,000, and Chintu-Rs 80,000. Abha will bring Rs 48,800 and Bimal will withdraw Rs 5,800. Bank Balance-Rs 1,88,000. Note: Calculation of Capital of Partners in NEW FIRM: Chintu's Capital, Total Capital of the New Firm `=Rs 80,000xx5//1=Rs4,00,000` Abha's New Capital `=Rs4,00,000xx5//10=Rs2,00,000,` Bimal's New Capital `=Rs4,00,000xx3//10=Rs1,20,000.` |

|

| 2719. |

Abhishek, Rajat and Vivek are partners sharing profits in the ratio of 5:3:2. If Vivek retires, the New Profit Sharing Ratio between Abhishek and Rajat will be– |

|

Answer» `3:2` |

|

| 2720. |

Abha and Bhrat whre partners. They shared profits and losses equally. On 1st April, 2014 their Capital Accounting showed balances of Rs3,00,000 and Rs2,00,000 respectively. Calculate the amount of profit to be destributed between the partners if the partnership Deed provided for Interest on Capital @10% p.a. and the firm earned a profit of Rs50,000 for the year ended 31st March, 2015. |

|

Answer» Solution :INTEREST on Abha's Capital = RS 3,00,000 `xx` 10/100= Rs 30,000 Interest on BHARAT's Capital = Rs 20,000= Rs 20,000 Total Interest on Capital = Rs 30,000 + Rs 20,000=Rs 50,000 Profit earned during the YEAR Rs 50,000 is equal to Interest on Capital, therefore, no amount of profit is left for distribution as the amount is sufficient only to pay the interest. |

|

| 2721. |

ABC Ltd.has Machinery written down value of which on 1st April, 2018 was Rs. 8,60,000 and on 31 st March , 2019 was Rs.9,50,000.Depreciation for the year was Rs.40,000 , In the beginning of the year , a part of machinery was sold for Rs.25,000 , which had a written down value of Rs.20,000 . Calculate Cash Flow from Investing Activities. |

|

Answer» Rs.1,25,000 |

|

| 2722. |

ABC Ltd. Has Machinery written down value of which on 1st April, 2018 was Rs 8,60,000 and on 31st March, 2019 was Rs 9,50,000. Depreciation for the year was Rs 40,000. In the beginning of the year, a part of machinery was sold for Rs 25,000, which had a written down value of Rs 20,000. Calculate Cash Flow from Investing Activites |

|

Answer» RS 1,25,000 |

|

| 2723. |

ABC Ltd. Has agreed to pay puchase consideration of ₹ 1,25,000 by issing fully paid debentures of ₹ 100 at ₹ 120 each . How will the purchase consideration be settled ? |

| Answer» Solution :Purchase CONSIDERATION will be SETTLED by ISSUING 1, 041 debentures and payment by CASH// chaque ₹ 80. | |

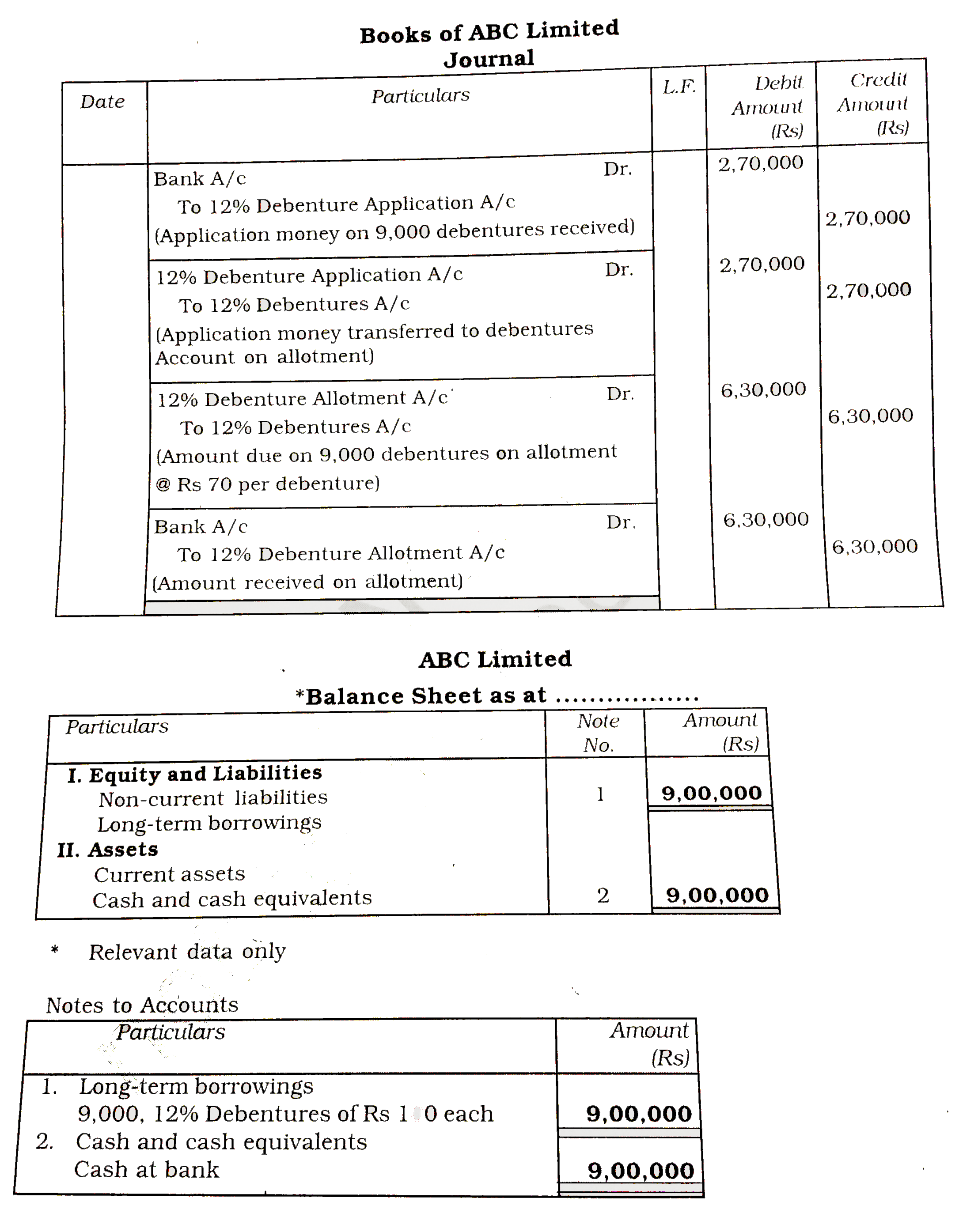

| 2724. |

ABC Lemited issured Rs 10,000 12% debentures of Rs 100 each payable Rs 30 on application and remaining amount on allotment.The public applied for 9000 debentures which were fully allotted and all the relevant allotment money was duly received . Give jornal entries in the books of ABC Ltd., and exhibit the relevent infromation in the blance sheet. |

Answer» SOLUTION :

|

|

| 2725. |

A,B,C and D were partners in a firm sharing profits in the tatio 3:2:3:2. On 1st April, 2016, their Balance Sheet was as follows: From the above partners decided to share the future profits in the ratio of 4:3:2:1. For this purpose the goodwiil of the firm was valued at Rs 2,70,000. It was also considered that: (i) The claim against Workmen Compensation Reserve has been estimated at Rs 30,000 and fixed assets will be depreciated by Rs 25,000. (ii) Adjust the capitals of the partners according to the new profit-sharing ratio by opening Current Account of the partners. Prepare Revaluation Account, Partners' Capital Account and the Balance Sheet of the reconsitatuon firm. |

|

Answer» SOLUTION :Loss on Revaluation- Rs 30,000, Partners' Capital ACCOUNTS A-Rs 3,92,000, B-Rs 2,94,000, C-Rs 1,96,00, D-Rs 98,000. Partners' Current Accounts, A-Rs 2,28,000 (Dr.), B-Rs 77,000 For Adjustment of GOODWILL: Dr. A's Capital A/c -Rs 27,000 and B's Capital A/c -Rs 27,000, CR. C's Capital A/c -Rs 27,000 and D's Capital A/c -Rs 27,000. |

|

| 2726. |

ABC Co. extends credit terms of 45 days to its customers. Its credit collection would be considered poor if its average collection period was. |

|

Answer» 30 DAYS |

|

| 2727. |

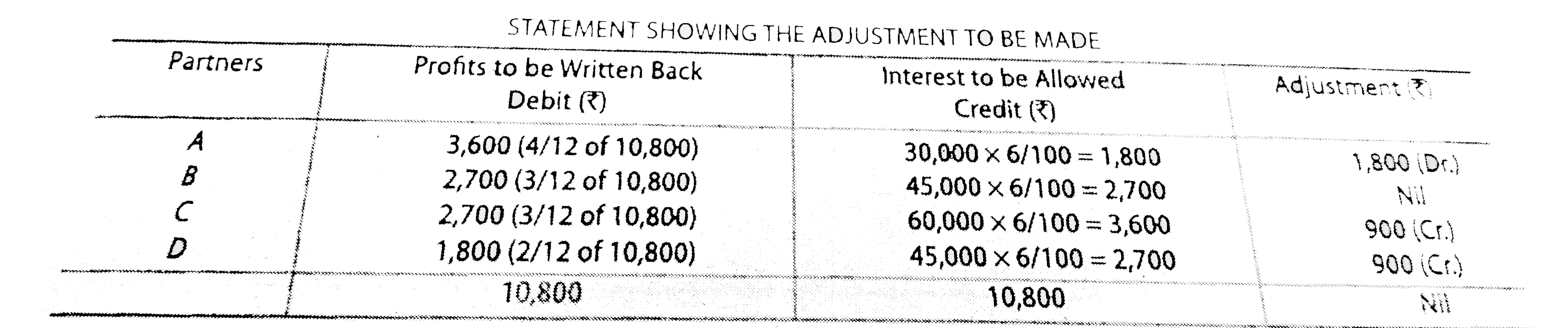

A,B,C and Dare partnerssharingsharingprofits and lossesin theratioof 4:3:3:2 and theirrespectivecapitalson 31st March2019wereRs. 30,000Rs, 45,000 Rs, 60.000and Rs. 45,000Afterclossingandfinalistingthe accounts, it wasnoticed thatinertest on capital@6%p.awasnotallowedinsted of afteringthesignedaccoutsit was decided to pass an adjusmententeryon 1stApril, 2019Creditingor debitingtherespective parthers's CApital?Current Accounts. |

Answer» SOLUTION : WORKING note : Interest on capital is caluated on theopenning in thequestionclosing of capitalare given, since theamount of profitcreditedto capitalshasnot beengiven ,It is notpossibleto openningcapitals thusit is assumed thatcapitalsof thepartners are fixed(i.e., sameon opening anddates ). interest ,on capital was RS. 10,8000 (a-Rs, 1,8000 ,B-Rs, Rs, 2,700 ,C- rs. 3,600and D- Rs, 2,700Due to theomissionofthisinterest an excessamoiunt of Rs. 10,800 as profithas beencreditted (distributed ) to thepartners in theprofit sharing ratiowhichshould have beendistributedin the capitalratio(i.e.,as interest on capital ), HENCE Rs.10,800should be writen back by debiting the partners in the profit-sharing ratio and thereafter distributedto them in the capital ratio .

|

|

| 2728. |

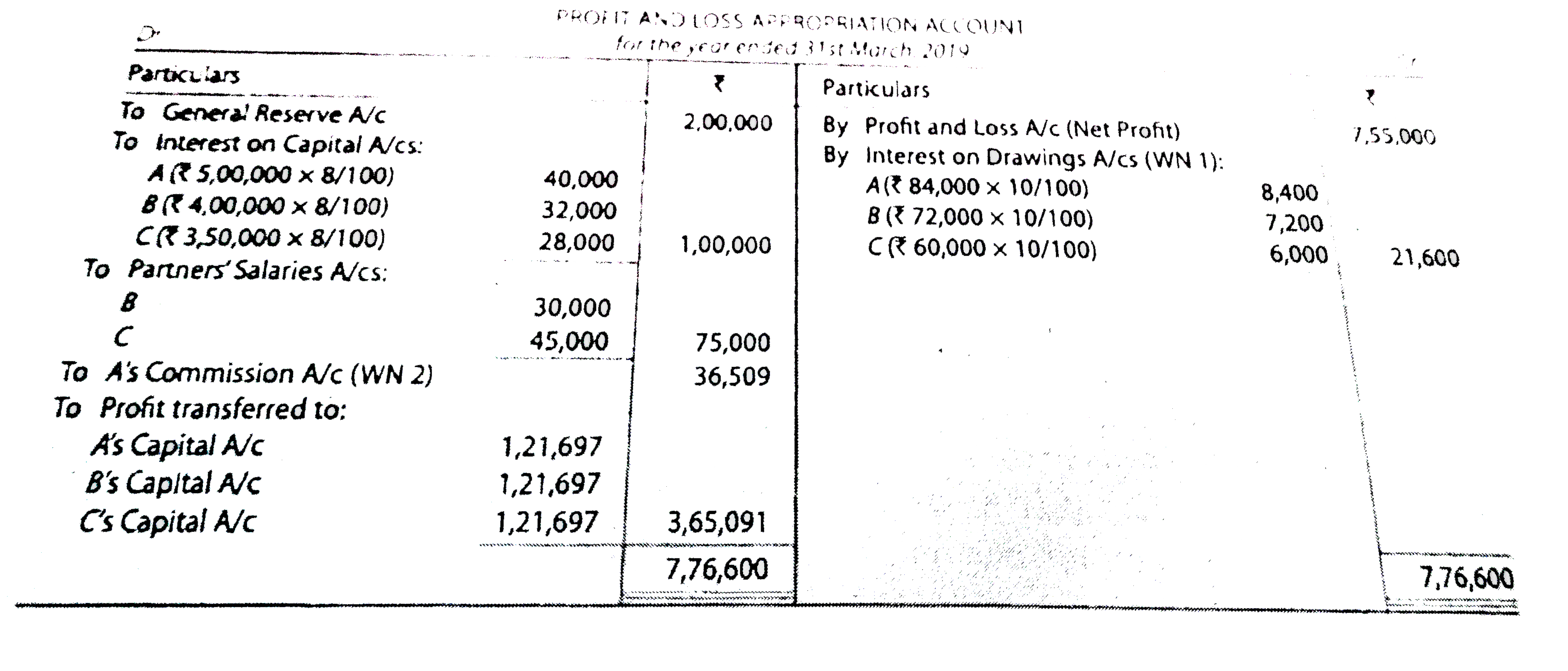

A.Band Carepartners in a firm,Accrdingto thepartnership Deed theparhters areentitledto draw up toRs. 7.000per month.On the1stday ofevry monthA .ABand CDrewRs. 7.000,Rs. 6.000and and RS. 5000 respectivelyinterestoncapitalsandintereston drawingare fixed@ 8 %and 10%respectivelyprofitfor theyearended31 st March2019was Rs. 7.55.000 outof whichand Rs.2.00.000are to berespectivelyand Ais toGereral ReserveB and Careto get salaryof Rs.30.000and 45.000p.arespectivelyand Ais toreceive commission @10% on disbuttable profits after charging such commission On 1st april2018vbalances of theircapitalaccountswere Rs. 5.00.000 ,Rs. 4.00.000and3.50.000respectively .Prepareprofitand loss appropriationaccount forth year ended31 st March, 2019adcapitalaccountsof partners in thebooksof thefirm . |

|

Answer»

WIDTH="80%"> WIDTH="80%">` (##TSG_ACC_XII_V01_C02_S01_015_S02.png" width="80%"> Workingnotes:- 1.interest on capitalintereston drawings are@ 8%and 10 %(andnot8% p.q and @ 10% p.a ) reaspectivelythereforethetimeisigored . 2.A'scommission `=10//110xx(Rs. 7,55,000+Rs. 21,600-Rs. 1.00.000-Rs.75.000-Rs.2.00.000)=rs. 36.509.` 3.Unless otherwisestatedinthedeedprofitfo theyearsi DIVIDED partners equally . |

|

| 2729. |

A,B C and D were partners in a firm sharing profits in the ratio of 4:3:2:1. On 1st january, 2015 , they admited E as a new partner for 1/10 share in the profits. E brought Rs. 10,000 for his share of goodwill premium which was correctly recorded in the books by the accountant. The accountant showed goodwill at Rs.1,00,000 in the books. Was the accountant correct in doing so? Give reason in support of your answer. |

|

Answer» Solution :No, the accountant was not correct in doing so. REASON: Since the NEW partner has brought his share of goodwill incash aganists self generated goodwill, it connot be RECORDED in the books of account. Only purchased goodwill can be recorded in the books of account as PER AS-26. |

|

| 2730. |

AB Ltd. invited applications for issuing 1,00,000 equity shares of Rs. 10 each. The amount was payable as follows : {:("On Application","Rs. 3 per share"),("On Allotment","Rs. 3 per share"),("On First and Final Call","Rs. 4 per share"):} Applications for 1,50,000 shares were received and pro-rata allotment was made to all applicants as follows : Applications for 80,000 shares were allotted 60,000 shares on pro-rata basis. Applications for 70,000 shares were allotted 40,000 shares on pro-rata basic. Sudha, to whom 600 shares were allotted out of the group applying for 80,000 shares failed to pay the allotment money. Her shares were forfeited inmediately after allotment. Asha, who had applied for 1,400 shares out of the group for 70,000 shares failed to pay the first and final call. Her shares we e also forfeited. Out of the forfeited shares 1,000 were re-issued @ Rs. 8 per share fully paid-up. The re-issued shares included all the forfeited shares of Sudha. Pass neccessary journal entries to record the above transactions. |

| Answer» SOLUTION :Amount received on ALLOTMENT RS. 1,48,800. Amount received on first call Rs. 3,94,400. Amount TRANSFERRED to Capital RESERVE Rs. 2,800. | |

| 2731. |

A.B C and D arepartnersin afirmsharingprofitsas 4:3:2:1 respectively . Itearneda neetprofitofRS. 1,80,000for theyear ended31st March ,2019 as per the partnershipDeedtheyareto chargeda commission@20%of theprofitaftercharging suchcommissionwhichtheyeill shareas 2:3:2:3. you arerequiredto showappropritionof profits amongthepatners . |

|

Answer» SOLUTION :Commissionpayableto THEPARTNERS`=20//120xxRs.30,000 `WHICHWILL be shared as :A-Rs. 6,000 :B-Rs.9,000 ,C-,C-Rs. 6,000 andD-Rs. 9,000 , shareof PROFIT,A 60,000 ,B-Rs.5,000 ,CRs. 30,000 andD-Rs. 15,000. |

|

| 2732. |

A,B and C were partners sharing profits and losses in the ratio of 7:4:3. On 1st April, 2018, D was admitted into partnership for 1/10th share in profits. D belongs to economically weaker section of the society and was admitted withour contributing any amount for his share of capital and goodwill. On the same date, A retired from the firm. A and B decided to donate old furniture of firm to an orphanage. Identify the values involved. |

|

Answer» (II) Fulfilling social responsibility; By donating OLD furniture to the orphanage. (iii) Transparency and FAIRNESS: By distributing accumulated PROFITS and Losses among old partners.] |

|

| 2733. |

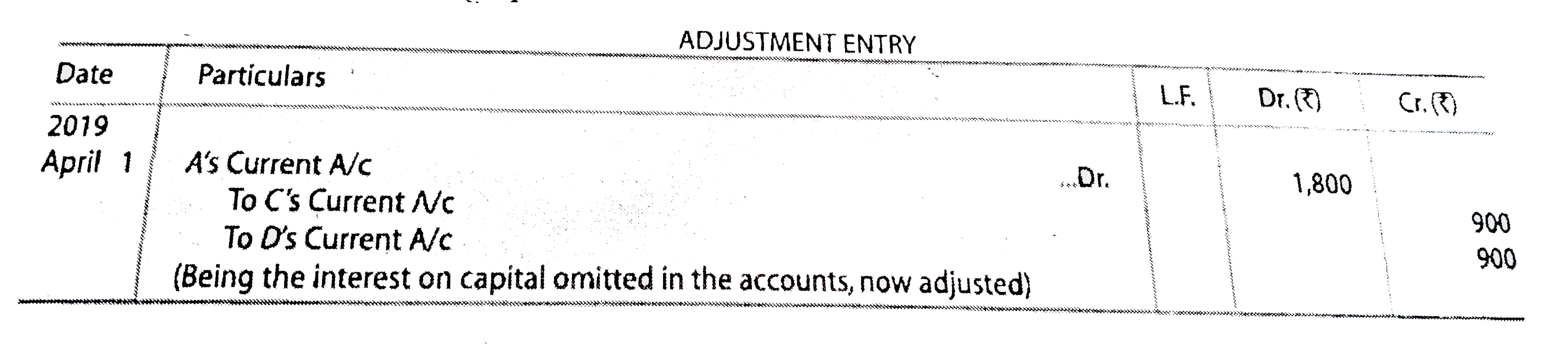

A,b and C were partners. They sarted business in one of the remote tribal areas of Odisha. They were interested in the development of the trible community by providing good education and health. On 31st March, 2013 after making adjustments for profits and drawings their capitals were A-Rs 4,00,00, B-Rs 3,00,00 and C-Rs 2,00,000. The drawings of the partners were A-Rs 4,000 per month, B-Rs 3,000 per month and C-Rs 2,000 per month. The profit of the firm for the year ended 31st March, 2013 was Rs 6,00,000. Subsequently, it was found that the interest on capital @6% p.a. due had been omitted. Showing your working notes clearly, pass neacessary adjustment entry for the above. |

|

Answer» SOLUTION :DR. C's Capital and Cr. A's Capital A/c by Rs 6,720. Note: OPENING Capital, A-Rs 2,48,000: B-Rs 1,36,000: C-Rs 24,00. |

|

| 2734. |

AB & Co. has 50 partners. It wants to admit a new Partner. Can it do so ? |

|

Answer» Yes |

|

| 2735. |

A,B and C were partners, sharing profits in the ratiio of 3:1:1. B died on 1st June, 2018 and as per his will, Rs 1,00,000 is to be donated to a society 'Clean Yamuna River'. What values are conveyed? |

|

Answer» |

|

| 2736. |

AB & Co. has 50 partners . It wanted to admit a new partner , Can it do so ? |

|

Answer» Yes. |

|

| 2737. |

A,B and C were partners in a firm sharing profits in the ratiio 3:2:1. They admitted D as a new partner for 1/8th share in he profits, which he acquired 1/16th from B and 1/16th from C. Calculate the new profit-sharing ratio of A,B, C and D. |

|

Answer» Solution :NEW profit-sharing ratio of A,B C and D is `48:26:10:12 or 24:13:5:6.` A's SHARE after D's ADMISSION = 3/6 or 48/96. B's share after D's admission = 2/6-1/16=26/96. C's share after D's admission = 1/6-1/16 = 10/96. D's share = 1/16 + 1/16=2/16or 1/8. |

|

| 2738. |

A,B and C are three partners in the firm , sharing in the ratio 2 : 2 :1. B retires from the firm on 31 st March, 2019 . The firm decides not to raise Goodwill Account . What entry will be passed in the books at the time of retirement of B for the goodwill? |

|

Answer» Dr. GOODWILL A/C , B's Capital A/c. |

|

| 2739. |

A,B and C are sharing profitsand losses in theratio of 5:3:2. Theydecided to share future profits and losses in the ratio of 2:3:5 witheffect from 1st April, 2019.They also decide to record the effect of the followingrevlautions withoutaffectingthe bookvalues of theassets and liabilities by passing an AdjustmentEntry : Pass necessarySingleAdjustment Entry . |

|

Answer» Solution :Calculationof NetEffect of Revalution: `{:(,,"₹"),(("i"),"Increase in VALUE of Lndand Building", "50,000"),(("ii"),"Decrease in amountof Sundry Creditors ","50,000"),(("iii"), "Decrease in valueof Plant and Machinery","(10,000)"),(("iv"),"Incrase in the amount of Outstanding Expenses","(15,000)"),(,"Gain (Profit) on Revalution",overlineunderlineunderline"30,000"):}` Step.2 Calculationof SACRIFICE/(Gain) of share: `{:(,,"A","B","C"),(("i"),"Old share", 5//10,3//10,2//10),(("ii"),"New share", UNDERLINE(2//10),underline(3//10),underline(5//10)),(("iii"), "Sacrifice/(Gain)(i)- (ii)",underlineunderline(3//10),underlineunderline(...),underlineunderline(-3//10)),(,,"Sacrifice",,"(Gain)"):}` Step. 3 Calculationof Proprtionate Amountof share of Gain (Profit) on Revaluation. A's Sacrified share `= 3/10xx ₹ 30,000 = ₹9,000,` C's Gained Share `= 3 xx 10 ₹30,000 = ₹ 9,000`. |

|

| 2740. |

A.B and C shared profits and losses in the ratio of 3:2:1 respectively. With effect from 1st April, agreed to share profits equally. The goodwill of the firm was valued at t 18,000. Pass necessaryJournal entries when: (a) Goodwill is adjusted through Partners Capital Accounts, and (b) Good raised and written off. |

|

Answer» (b) (i) Dr. Goodwill A/c - ₹18,000. Cr. A's Capital A/c - ₹9000; B's Capital A/c - ₹ 6000 andC's Capital A/c-₹3000. (ii)Dr. A's Capital A/c- ₹6,000; B's Capital A/c- ₹6,000 and Cs Capital A/c- ₹6,000; Cr. GoodwillA/c- ₹ 18,000. |

|

| 2741. |

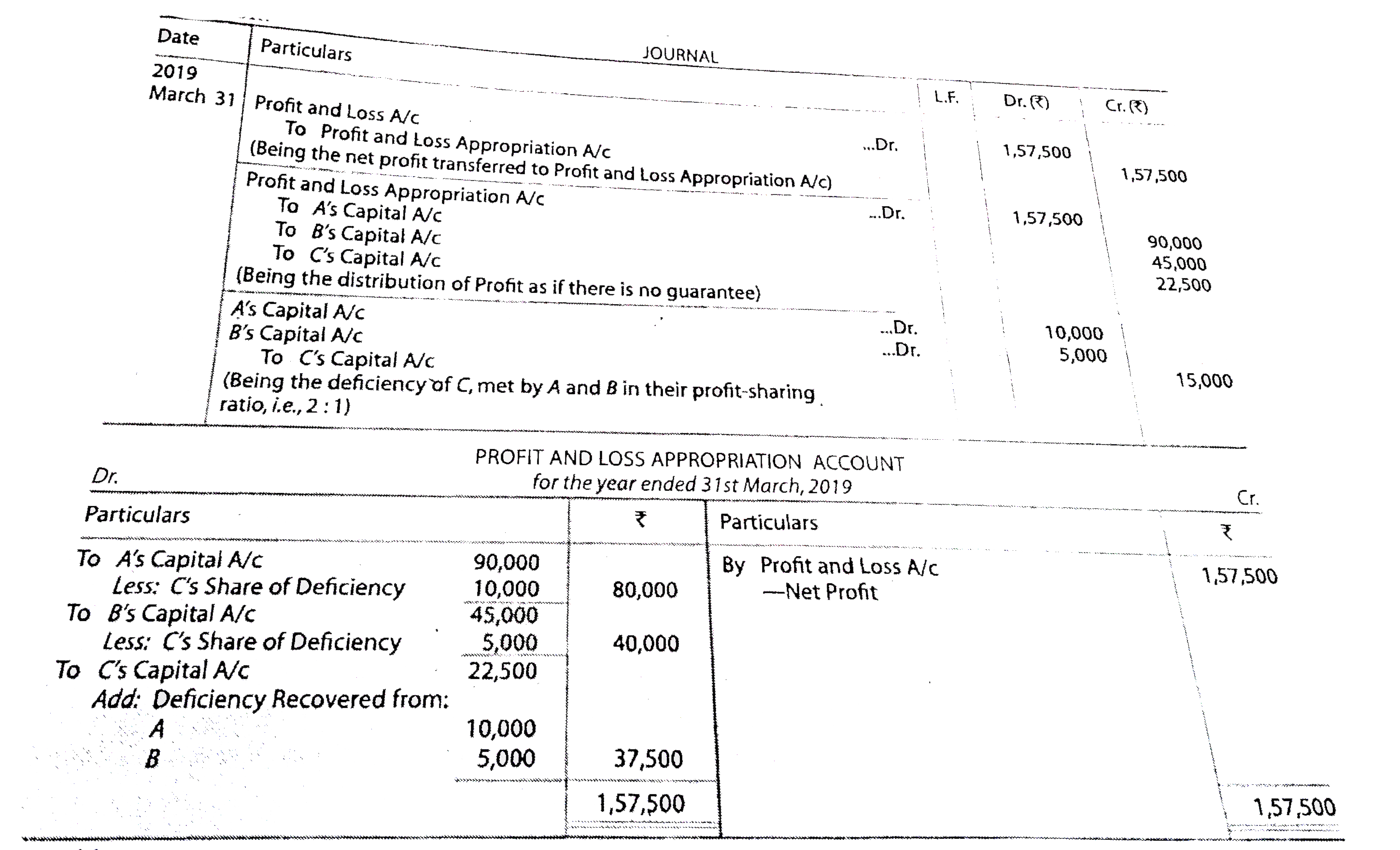

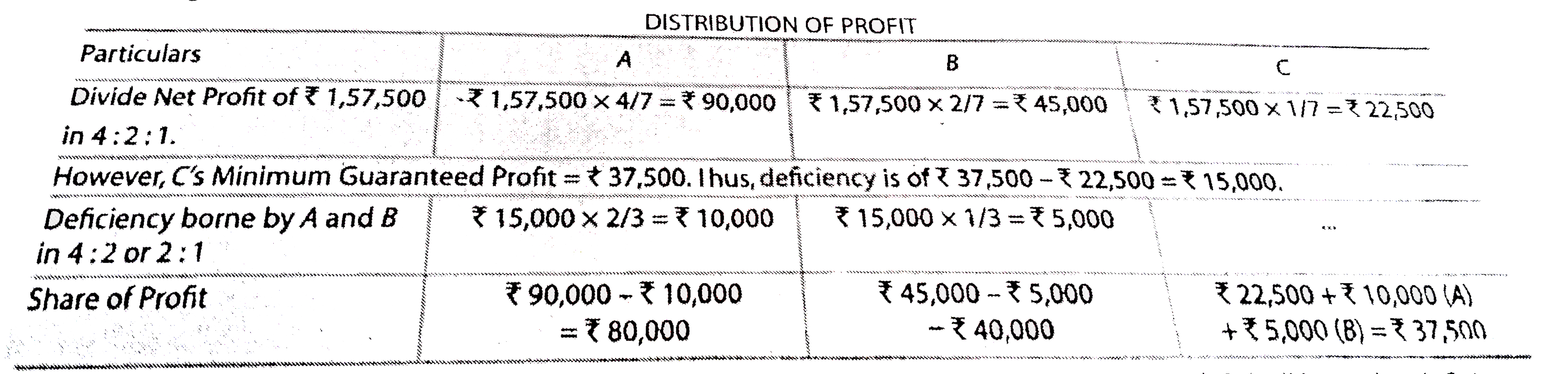

A,B and Cwerein partnershipsharingprofitand lossesin theratioof4:2:1it wasprovidedthatC'sshareon profitforayearwouldnot belessthanRs. 7,500profitfor theended31st March, 2019Amountedto Rs. 31,500 you arerequiredto showthe appropriationamongthe partnerstheprofitandlossappropritaitonAccount isnitrequired. |

| Answer» SOLUTION :shareofprofitA -RS. 16,000 ,B'sRs. 8,000.C's 7,500 | |

| 2742. |

A,B and C are partners sharing profits in the ratio of 5 : 3 : 2 . They decided to share future profits in the ratio of 2 :3 : 5 with effect from 1st April , 2019 , They also decided to adjust the following accumulated profits, losses and reserves without affecting their book values , by passing an adjustment entry : Profit and loss A/c Rs. 15,000 , General Reserve Rs. 60,000 , Advertising Supense A/c Rs. 30,000. The necessary adjustment entry will be : |

|

Answer» Dr . C's CAPITAL A/c and A's Capital A/c with Rs.13,500. |

|

| 2743. |

A,Band C arepartnersin afirmsharingprofits in theratioof 4:2:1 itisprovidedthatC'sshareinprofitwouldnotbe lessthan Rs. 37,50profitand lossAppropriatonAccount . |

Answer» Solution :  2.sinceno specificIs GIVENIN whichthedeficiencyis tobe borneit MEANS A and C SHALL bearthedeficiencyin their SHARING ratio i.e., 4:2 or 2:1. |

|

| 2744. |

A,B and C arepartnerssharingprofits and lossesin theratioof 2:2:1resptivelyA isentited to acommissionfo 10%on thenetprofitNetprofitfor theyearis Rs. 1,00,000. Determinethe amount ofcomissionpayableTo A . |

| Answer» SOLUTION :Commissionpayable TOA -RS, 11,000 | |

| 2745. |

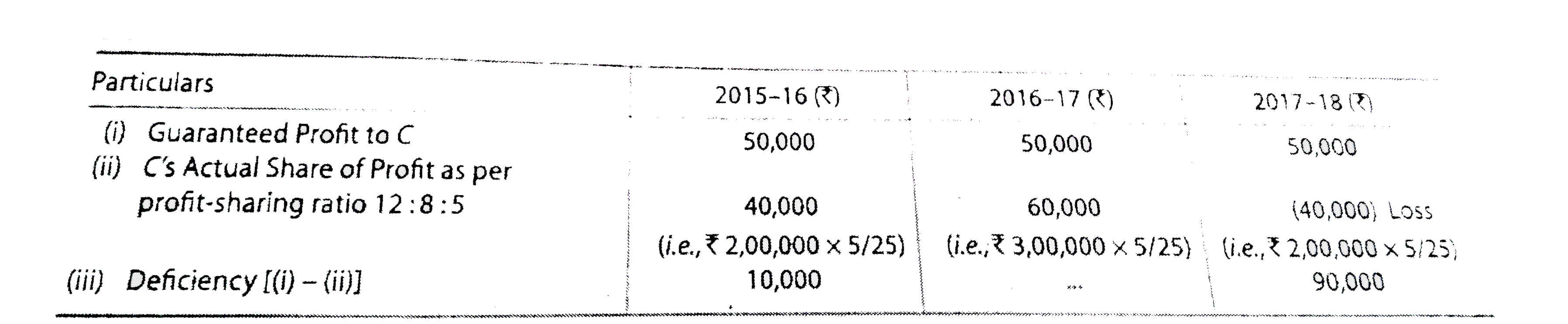

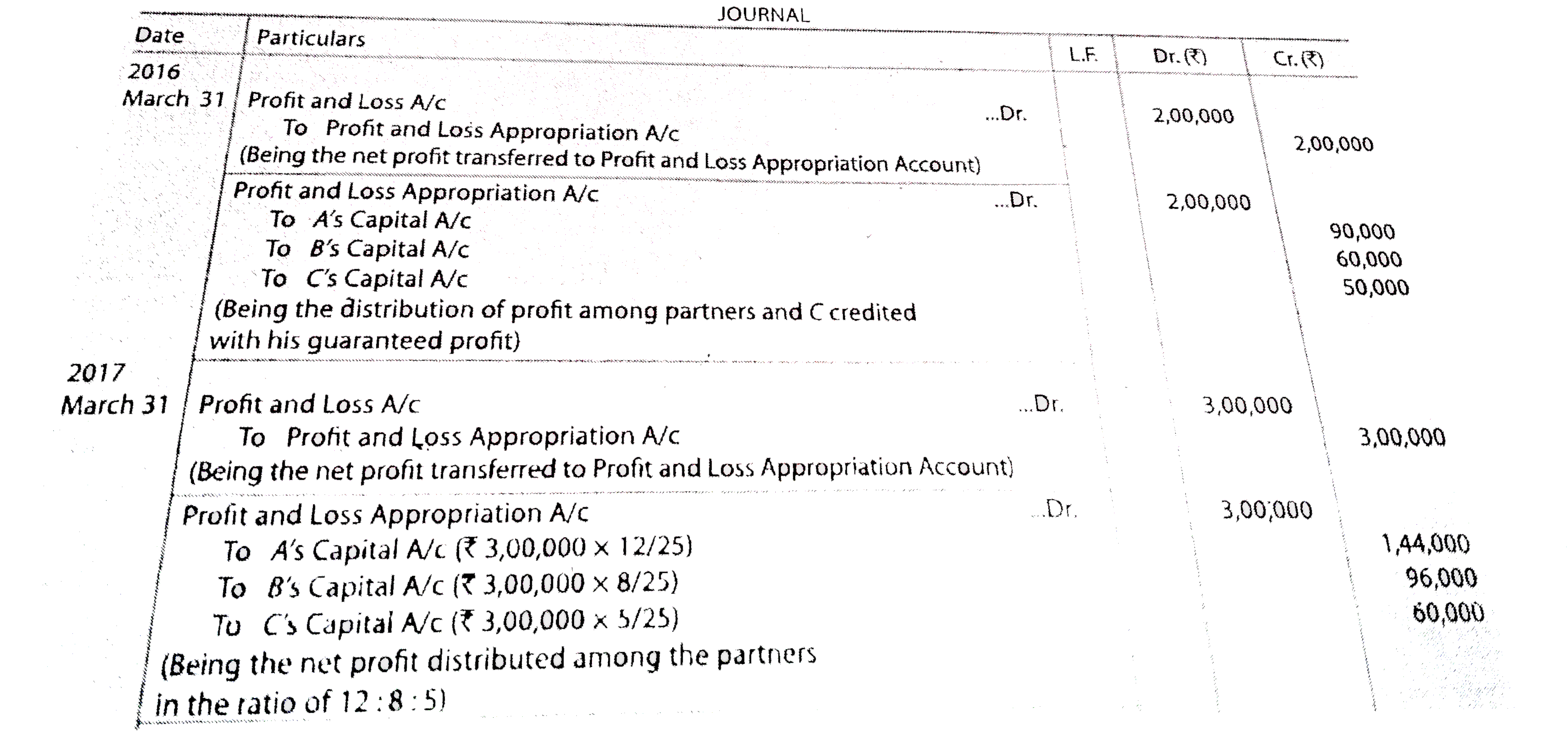

A,B and Care partnersin a firmsharingprofitsand lossesin theratioof 12: 8:5partner CIs Guaranteeda minimumprofitofRs, 50,000 p.abythe firm, theprofitand Lossesof theyearsended31st Marchwere: 2016 ,:- ProfitRs. 2,00,000 , 2017 -profitRS. 3,00,000and2018-LossRs. 2,00,000 Passnecessaryjournalenteriesin thebooksof thefirm . |

Answer» SOLUTION : Thedeficiency in C'sshareof profitis tobeborneby thefirmthusoutprofitof thefirmC'scapital Accountwill becresitedwithminimumGuaran teedprofitor hisshareof profitwhichever ishhgherandtherefore ,Balancewillbedistributedto A and Bin theirprofit- sharingratio in caseof LOSSWILL bedebitedro PARTNERS 'capitalAccountsand thereafter,deficiency inguaranteedpartner'ssharewillbedebitedtoreamainingpartners 'CapitalAccounts.

|

|

| 2746. |

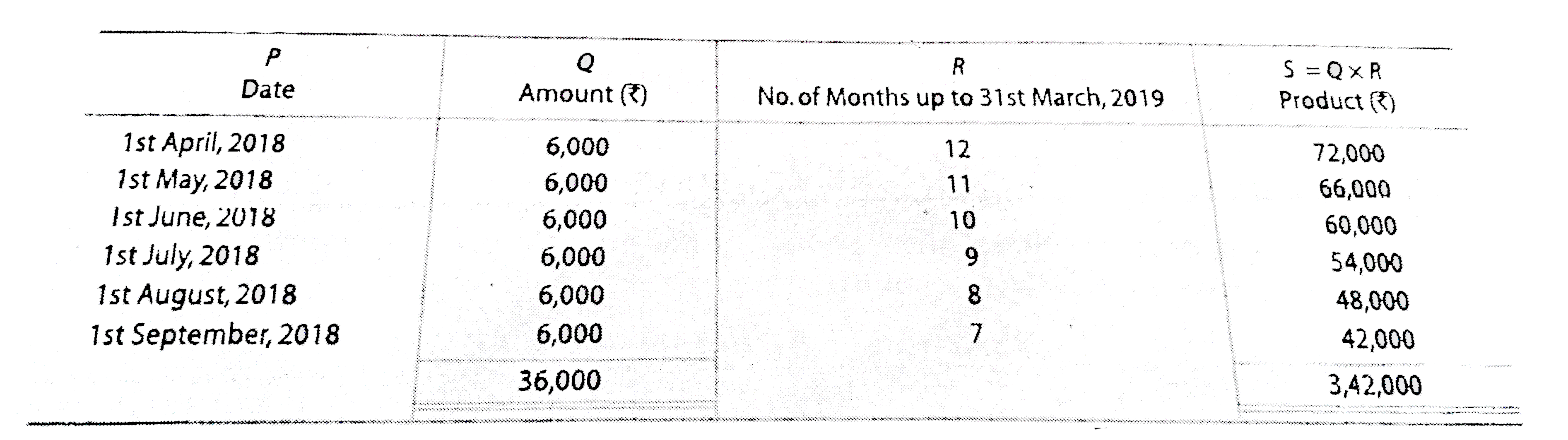

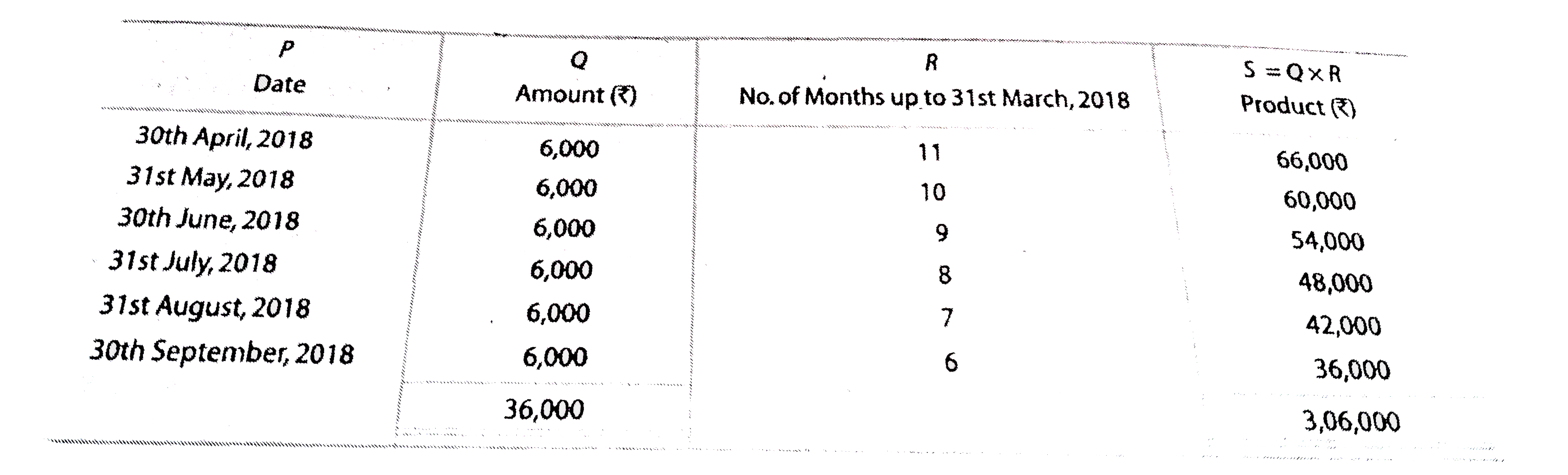

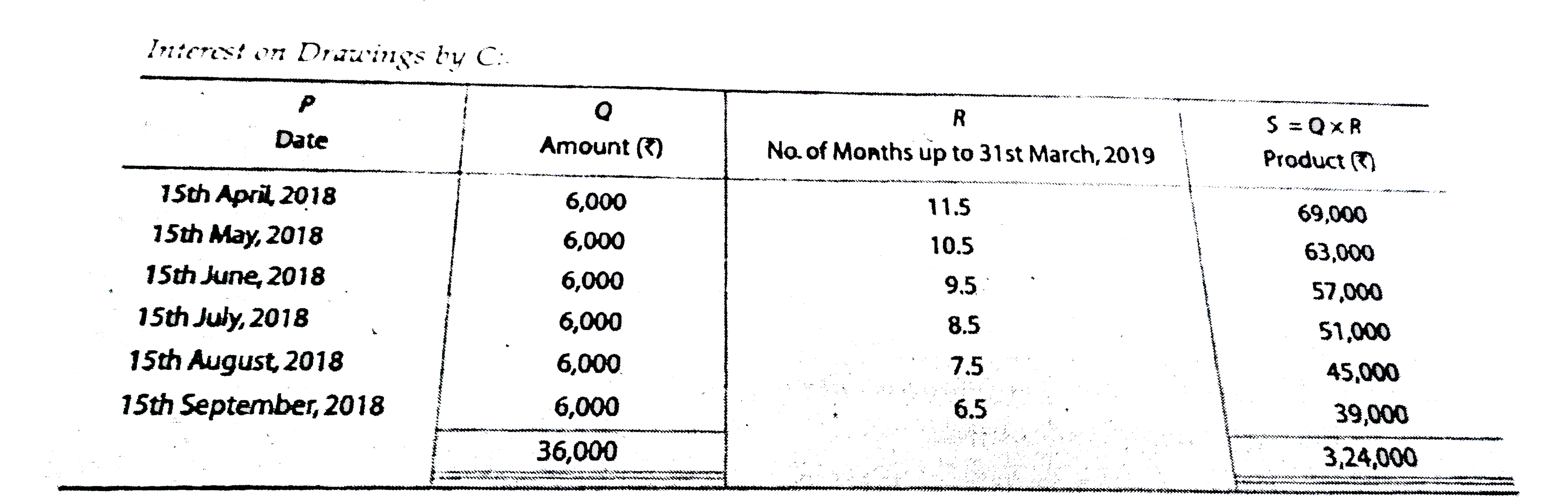

A.Band CarepartnersSharingprofitsequally.AdrewregularlyRs. 6.000in thebeing ofevery monthfor thesixmonthfor thesixmonthseneded30 thSeptember , 2018BdrewRegularlyRS. 6,000 inthemiddleofeverymonth forthesixmothsof the six monthsended30 saptember2018 XCdrew regularlyRs. 6000 inthe middleofevery monthfor thesix monthsended30 th september . 2018Calculatweinteresti drawings@ 5%p.awhentha booksareclosedon 31st Marchevery year . |

Answer» Solution : intereston Rs. 3,42,000 @ 5% p.a forone month `= Rs.3,42,000xx(5)/(100)XX(1)/(12)=Rs. 1,425`. alternativelyinterest maybecalculated for 9.5months [(12 months+7 months )/2] @ 5%p.a onRs`. 36,000 xx(5)/(100)xx(9.5)/(12)=Rs.1,425`  interestOn Rs. 3,06,000@ 5%p.afor onemonth = Rs. 1,275. alternatively interestmay becalculated for 8.5months[(months+6 months )2] @5% p.a On` Rs. 36,000 =Rs. 36.000xx(5)/(100)xx(8.5)/(12)=Rs. 1,275.`  intereston Rs. 3,24,000 @ 5%p.a FOR1 month =Rs. 1,350 alternatvely , interestmay becalculated for 9 months [(11.5 months +6.5 months )/2]` @5%p.aon Rs. 36,000 =Rs. 36,000xx(5)/(100)xx(9)/(12)=Rs. 1,350.` Situation 4.amount is withdrawnin thebegining of eachquarter during the year, interest ischargedon thewhole amountfora period of `7^((1)/(2))`months *. intereston drawings = `("total Drawings "xx"Rateof interest ")/(100)xx(7^((1)/(2))/(12)` *Average period `=("12 months +3months ")/(2) =("15 months ")/(2)=7^((1)/(2))`months . situation5.if fixedamount is withdrawnat themiddleof each quarter duing the year . interest is CHARGED on thewhole amountfor a period of 6 months *. interest on drawings `=("Total Drawings "xx"Rate of interest ")/(100)xx(6)/(12)` * Average period `=(10.5 months +1.5Months )/(2)=(12 months )/(2)=6` months . situatio 6.of fixedamount iswithdrawingat theendquarter the year , interest is chargedon thewholeamountfor aperiodof `(4^(1/2))` months * * average period`=("9 months+0 Months ")/(2)=("9 months ")/(2) =4^(1/2)` months . |

|

| 2747. |

A,B and C are partners in a firm sharing profit and lossed in the ratio of 3 : 2 : 1 . B died on Ist April, 2018 . C, son ofB, is of the opinion that he is the rightful owner of his father's share of profits, and the profis of the firm should now be shared between A and C by giving reason. |

| Answer» Solution :C is not correct in his claim. Unless agreed , new profit SHARING ratio of the CONTINUING PARTNERS remains same as their old proft-sharing ratio i.e., 3 : 1 . | |

| 2748. |

A,B and C are partner's in a firm. If D is admitted as a new partner: |

|

Answer» OLD FIRM is dissolved |

|

| 2749. |

A,B and C are partneres sharing parofits and losses in the ratio of 2:3:5. On 31st March, 2019 they admit D into the partnership and decided to use 10% of the profits every year in providing dringking water in schools, where required. What values are being converyed by them? |

|

Answer» |

|

| 2750. |

Aakriti and Bindu entered into partnership for making garment on April 01, 2016 without any Partnership agreement. They introduced Capitals of Rs. 5,00,000 and Rs. 3,00,000 respectively on October 01, 2016. Aakriti Advanced. Rs, 20,000 by way of loan to the firm without any agreement as to interest. Profit and Loss account for the year ended March 31 2017 showed profit of Rs, 43,000. Partners could not agree upon the question of interest and the basis of division of profit. You are required to divide the profits between them giving reason for your solution. |

|

Answer» |

|